9 key differences between GRI Standards and BRSR for sustainability reporting

- Pawan N V S

- Sep 4, 2024

- 5 min read

Updated: Aug 26, 2025

Introduction

Global Reporting Initiative Standards (GRI Standards) are the first and the most widely used standards by businesses for sustainability reporting. The work on these standards started way back in 1997 and these standards continue to evolve even today. BRSR reporting framework was adopted by SEBI from FY 2022–23 as an improved version of earlier non-financial disclosure frameworks used by businesses listed in Indian stock exchanges. Reporting mandate under the BRSR framework is being expanded every year to bring more businesses in its ambit.

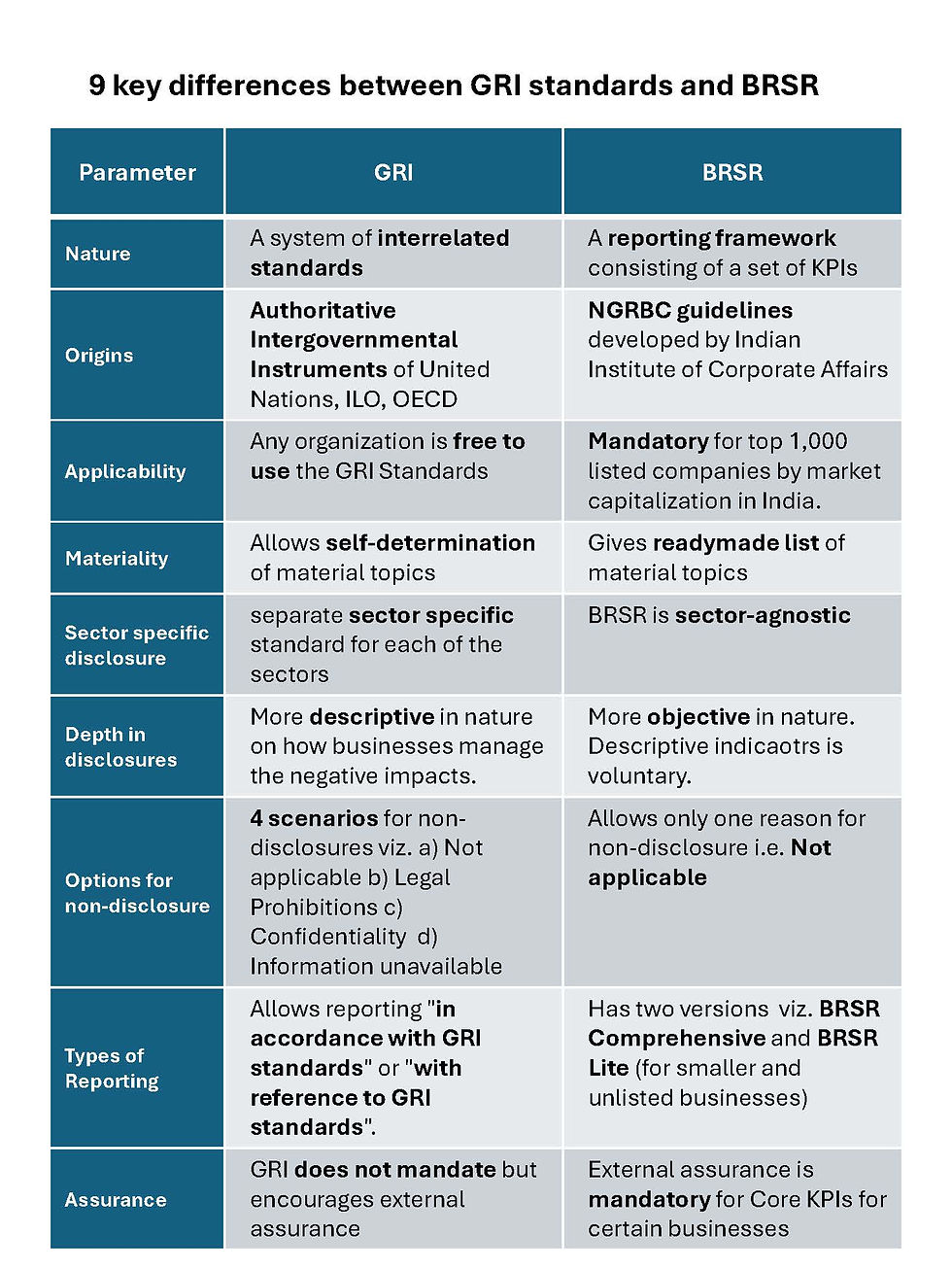

While both GRI and BRSR aim to disclose a business’s approach and performance regarding responsible operations, a closer examination reveals nine key differences between these two reporting frameworks.

1. Nature

GRI are a system of interrelated standards that specify the disclosure requirements and reporting principles that the businesses must comply with to publicly disclose their “significant impacts on economic, environment and people, including impact on their human rights.”

BRSR is a sustainability reporting framework consisting of Key Performance Indicators (KPIs) to serve as a tool to assess where the businesses are in their journey of responsible business conduct.

2. Background Origin

GRI has been developed by muti-stakeholder experts based on various international agreements of the United Nations (UN), International Labor Organization (ILO) and Organization for Economic Co-operation and Development (OECD). It also takes references from various national and international guidelines on specific topics.

BRSR has its roots in the National Guidelines on Responsible Business Conduct (NGRBC) published by the Indian Institute of Corporate affairs in 2019. The 9 principles of the NGRBC form the bedrock of this sustainability reporting framework.

3. Applicability

GRI has been developed in public interest. It is a global standard and any business that has to report its sustainability related information under any regulation is free to use or refer to the GRI Standards.

BRSR framework has been developed keeping in view the relevance to the Indian market context. The KPIs have been designed based on Indian laws applicable to businesses operating in India. However, it also ensures that the published data is globally comparable.

4. Thrust on Materiality

GRI gives a lot of thrust on materiality and determination of material topics. The standards define material topics as “topics that represent the most significant impacts of the business on economy, environment and people” (e.g. GHG Emissions, Corruption). GRI 3: Material Topics provides step by step guidance on how to determine material topics. The businesses need to document the process of determining material topics. It expects businesses to continually and independently, keep assessing its actual and potential negative impacts and add new material topics.

BRSR framework provides a readymade list of material topics based on the NGRBC principles. There is no explicit requirement for the businesses to go beyond the framework and identify or report on other sustainability topics. In certain KPIs, it refers to the definition of materiality as in the SEBI LODR guidelines.

5. Sector specific disclosures

GRI identifies various sectors of businesses and has separate sector specific standard for each of the sectors (e.g. oil and gas, coal, mining, etc.) Sector standards enlist the likely material topics for the businesses operating that sector. Businesses need to report/disclose on each of the listed material topics, if it falls in the scope of the sector standard.

BRSR is sector-agnostic. All businesses need to report on every KPI listed in the framework. However, it allows businesses to report “Not Applicable” if any of the topics is not relevant to their business scenario along with reasons for the same.

6. Depth in disclosures

GRI standards requires the business to explain in depths as to how it manages each of its material topics. If a material topic has been identified, it has to describe a) the actual and potential, negative and positive impacts b) describe the activities or business relationships involved with the negative impacts c) describe its policies or commitments regarding the material topic d) describe actions taken to manage the topic and related impacts e) report information about the effectiveness of the actions taken and f) describe how stakeholders were engaged and kept informed of the actions taken.

BRSR disclosures are more objective in nature. The essential indicators are a combination of specific data and descriptive explanations on the KPIs. Leadership Indicators section requires descriptive explanations of the business’s top management approach to the sustainability topic. This section is, however, voluntary at present.

7. Options for non-disclosure

GRI makes it mandatory to disclose all “requirements” of any Topic standard and encourages to also report “recommendations” of the standard. However, GRI stipulates 4 scenarios for non-disclosures: a) Not applicable b) Legal Prohibitions c) Confidentiality constraints and d) Information incomplete/unavailable. Points (c) and (d) can be used as an exception only. Such a reason should accompany an explanation of the reasons.

BRSR guidance note stipulates that the business need not disclose the certain KPIs if such disclosures are not applicable to the industry. It does not give any other scenario/option for non-disclosure.

8. Types of Reporting

Under GRI, businesses can choose to report either “in accordance with GRI standards” or “with reference to GRI standards”. The former demands compliance with all the 9 requirements as stipulated in GRI 1: Foundation 2021. Reporting “with reference to GRI standards” means businesses can independently use select GRI Standards, or parts of their content, to report information about specific topics for specific purposes. In this case, GRI standard acts as a guidance to assimilation of required data and reporting of the information.

BRSR also has 2 versions, BRSR Comprehensive and BRSR Lite. BRSR Lite is a subset of the comprehensive version which can be used by listed smaller businesses and unlisted businesses to make their sustainability disclosures. BRSR Lite identifies the most significant and contains simplified disclosures. BRSR Lite is an accessible entry point for responsible reporting.

For an overview of the BRSR framework, see the video from the author:

9. Assurance

GRI does not mandate businesses to obtain external assurance when reporting in accordance with the GRI Standards but is encourages to do so to enhance the credibility of sustainability reporting.

BRSR specifies two levels of assurance viz. reasonable assurance and limited assurance. A reasonable assurance is mandatory for Core KPIs for top 250 businesses by market capitalization in India (for FY 2024–25). SEBI encourages other businesses whether adopting BRSR comprehensive or BRSR Lite, to voluntarily obtain third party assurance of their disclosures.

Conclusion

GRI aims to bring transparency and accountability in the manner in which businesses manage their impact on economy, environment and people. It is based on the premise that sustainability should progress from being a statutory compliance to a significant shift in how businesses operate. GRI tries to elicit an unwavering commitment from businesses worldwide in adopting sustainable practices.

BRSR’s approach is to reduce the complexity and subjectivity associated with reporting non-financial disclosures. The idea is to standardize the reporting so that it be made comparable and certain industry benchmarks can be created. Inclusion of mandatory assurance is a bold move to ensure all businesses fall in line. This approach is justified in a country which still needs to achieve maturity in sustainability reporting.

References

GRI: Consolidated Set of GRI standards

SEBI: Guidance Note for Business Responsibility & Sustainability Reporting Format

SEBI: Business Responsibility & Sustainability Reporting Format

Ministry of Corporate Affairs: National Guidelines on Responsible Business conduct

Comments